Directed trusts have emerged since 1986 as an important and yet arguably underutilized estate planning and trust administration tool, offering unique advantages in terms of trustee liability, cost efficiency, and potential tax savings. By implementing directed trusts, savvy families and their advisors can leverage this strategy to achieve long-term estate planning and financial goals.

Directed trusts have emerged since 1986 as an important and yet arguably underutilized estate planning and trust administration tool, offering unique advantages in terms of trustee liability, cost efficiency, and potential tax savings. By implementing directed trusts, savvy families and their advisors can leverage this strategy to achieve long-term estate planning and financial goals.

Understanding Directed Trusts

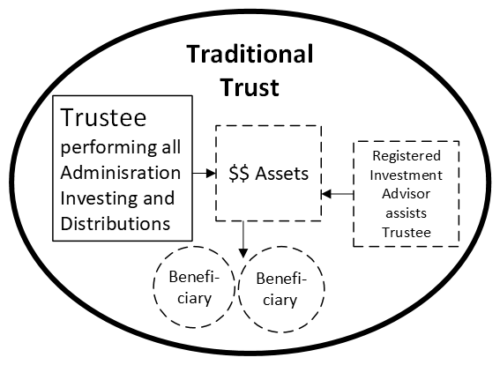

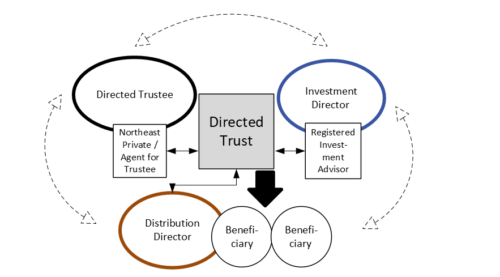

In a typical trust, the trustee is responsible for all administrative and investment decisions. A directed trust, on the other hand, separates the roles of a trustee into logical component parts. In a directed trust, the trustee is directed either by co-trustees or trust advisors, or, my preferred term, trust directors.

These roles can separated out:

- Directed Trustee: Handles the administrative duties, such as record-keeping, tax preparation, and accounting. The (Directed) Trustee can delegate the back office work to an administrative agent, such as Northeast Private Trustee Services. The Trustee does not need to sign off on investments or distribution of funds. The Trustee or its agent may be the coordinator of all trust fiduciary functions, without liability for how anything, except their own functions, are carried out.

- Investment Director or Trustee: Controls trust investment decisions, selecting and managing assets within the trust. An Investment Director usually works with a Registered Investment Advisor (RIA) to develop and implement the investment policy for the trust and to report to the beneficiaries. If permitted by the RIA’s internal rules, the RIA himself might serve as the Investment Director. There’s also nothing to prevent the trust grantor from being the Investment Director

- Distribution Director or Trustee: Makes distributions or directs the Trustee to make distributions. A Distribution Director will have the primary responsibility for the welfare of the trust beneficiaries within the terms of the trust, but, unless given the upper hand, is, for all intents and purposes, subordinate to the Investment Director if there are no assets, especially cash, to distribute.

This division of labor provides several benefits:

- Trustee Liability: One of the primary advantages of directed trusts is the potential limitation of trustee liability. By placing investment decisions on an independent advisor, the directed trustee’s exposure to investment liability is eliminated or significantly reduced. This can be particularly beneficial in complex investment scenarios or when dealing with high-risk assets. Likewise, if a trust places distribution decisions in the hands of an independent distribution advisor, then the Directed Trustee is not responsible for the time-consuming monitoring of the beneficiaries.Depending on state law, the Directed Trustee may bear limited responsibility, as in Massachusetts, to see that the Directors act in the best interests of the beneficiaries and comply with the trust agreement or, better yet, as is the case under New Hampshire law, is free of liability.

- Cost of Trustee Services: Directed trusts can offer cost savings not only by lowering the potential liability cost of serving as the Trustee, as we have just seen, but also by reducing the scope of services required from the trustee. Since the Investment Director handles the time-consuming investment decisions and the Distribution Director the beneficiary relations, the Directed Trustee’s fees should be lower, perhaps much lower, than the traditional trust trustee.

- Tax Savings in No-Income-Tax States: Some states that are favorable for directed trustees do not impose income tax on trusts. By strategically structuring the trust and selecting appropriate investments, it may be possible to minimize or eliminate income tax liability. For example, if the trust is domiciled in a no-income-tax state like New Hampshire and the investments generate capital gains, those gains will not be subject to state income tax unless there is an exception under tax law. Closely held stock, governed by the Investment Director, may be sold and the trust may pay only federal capital gains taxes, avoiding state taxes, provided the trust does not have source income in a state with an income tax and to the extent that no distributions are made to a beneficiary in a jurisdiction with a state income tax.

Key Considerations for Directed Trusts:

While directed trusts offer numerous advantages, it is crucial to carefully consider the following factors:

- Trust Agreement: The trust agreement must clearly outline the roles and responsibilities of the Directed Trustee and Directors or co-trustees. It should also specify the investment guidelines and any limitations on the investment advisor’s discretion. The instrument should require coordination between investment and directed or distribution trustees to avoid a conflict or impasse. The trust should clearly separate trustee responsibilities and remove the implication of any more responsibility than mere administration, investment or distribution as the case may be, and allow mediation, arbitration or judicial interpretation. We have learned these lessons from case law in Shelton v. Tamposi (NH, 2013) and Accident Insurance (4th Cir., 2022).

- Investment Advisor Selection: Choosing a qualified and experienced investment advisor is essential. The advisor should have a track record with the securities markets or a willingness to take the advice of an RIA. or some other specific investment, a deep understanding of the trust’s investment objectives, and a fiduciary duty to act in the best interests of the beneficiaries.

- Cost Considerations: While directed trusts may offer cost savings, it is important to weigh the potential benefits against the additional fees associated with preparing the trust instruments, possible attempts to assess income tax by state departments of revenue if one objective is to minimize state income tax (which may be the case with or without directed trust status).

- State Laws: The laws governing directed trusts vary by state. Some state laws expressly allow the use of directed trusts, e.g. New Hampshire where our branch office is located. Other states only recognize delegation of duties, which is largely untested as a liability shield for trustees. Be sure to consult with a trust and tax counsel to ensure compliance with local law, decide on a jurisdiction to operate within and to optimize the trust structure.

Directed trusts can be a powerful tool for estate planning, offering benefits such as reduced trustee liability, potential cost savings, and tax advantages in certain jurisdictions. To help evaluate whether a directed trust is right for your situation, please contact us.